“We’re still seeing a holding pattern across the market. Many projects originally expected to launch in 2025 were pushed to Spring 2026, and a number of those still aren’t showing signs of moving forward. The limited supply that is reaching the market is increasingly concentrated on end-user-driven product. On the rental side, completions are tied to construction timelines and tend to be less seasonal, though winter typically remains a slower period for absorption and move-ins.”” — Melissa Nestoruk, Product Development Specialist, MLA Canada

MARKET INSIGHTS - MARCH 2026

February continued the measured start to the year across presale and rental markets. Launch activity remained well below typical seasonal averages, with many projects originally anticipated for 2025 still showing limited signs of moving forward. The supply that is reaching the market is increasingly concentrated on end-user-driven townhome product, while higher-density launches remain constrained. On the rental side, completions increased as projects reached construction milestones, though leasing activity reflected typical winter seasonality. Overall, the market remains in a holding pattern, with both buyers and developers proceeding cautiously amid broader economic uncertainty.

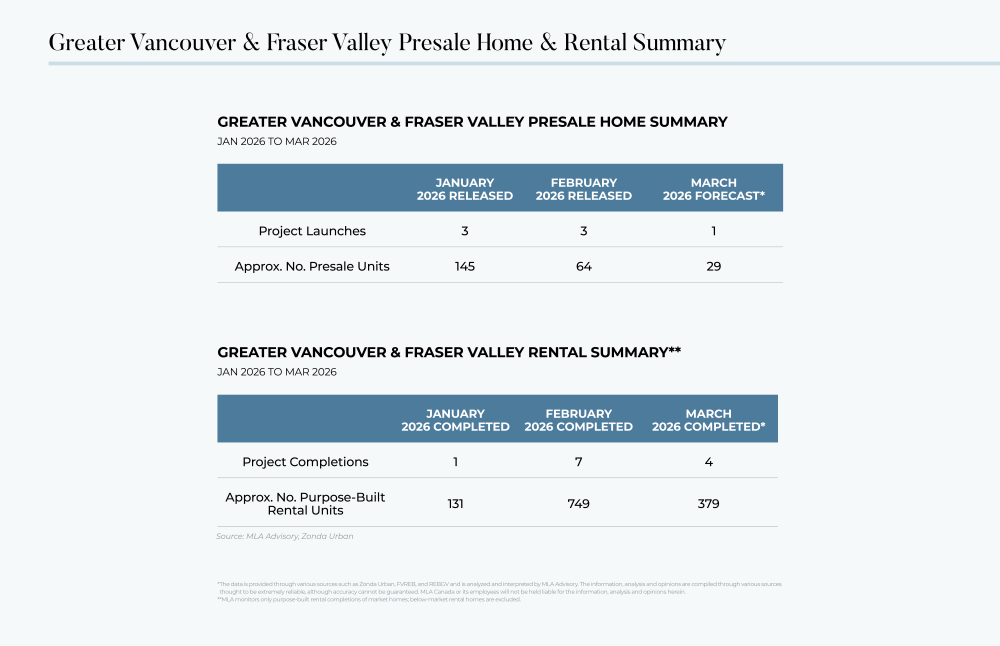

PRESALE SUMMARY

Presale momentum remains subdued, with limited new supply entering the market and activity largely focused on lower-density product. February releases were modest compared to historical norms, and March forecasts indicate continued restraint in launch volume. Buyer engagement remains selective, with demand centered on practical layouts, lifestyle-oriented locations, and pricing that reflects today’s competitive landscape. Developers continue to evaluate timing carefully, refining unit mix and strategy before advancing larger-scale projects.

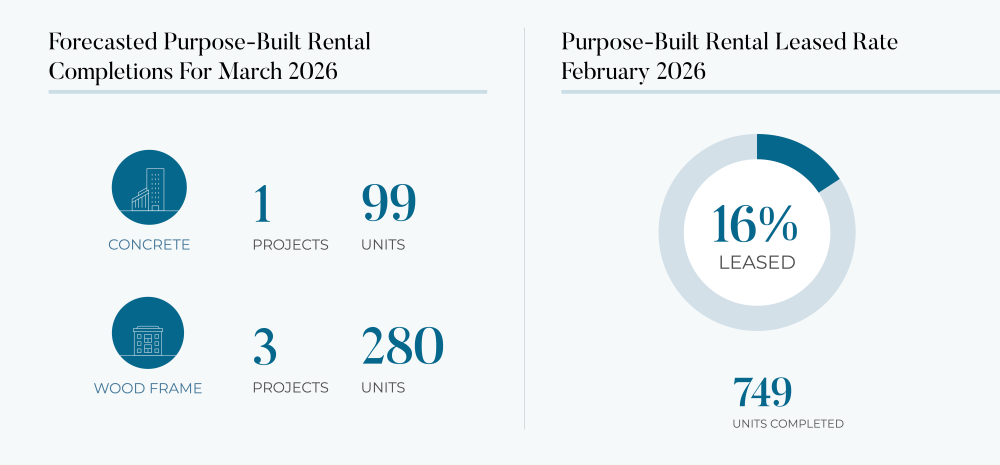

PURPOSE-BUILT RENTAL SUMMARY

Rental completions increased through February, largely reflecting construction timelines rather than a shift in market conditions. The majority of new deliveries were wood-frame mid-rise buildings, contributing to a steady expansion of available inventory. Leasing performance remained consistent with winter trends, with absorption progressing at a measured pace as tenants compare options and evaluate overall value. As additional projects complete in the coming months, competitive positioning and pricing alignment will remain critical to maintaining leasing velocity.

RESALE SUMMARY

Resale activity improved month-over-month in February across both Greater Vancouver and the Fraser Valley, though overall sales remain below long-term averages. Inventory levels continue to sit above historical norms, reinforcing negotiating power for buyers and placing gradual downward pressure on pricing. While new listings have moderated compared to last year, supply remains elevated relative to demand, contributing to a cautious but stable market environment. Broadly, resale conditions mirror presale trends, with measured activity, increased choice, and buyers proceeding deliberately rather than aggressively.

Coming soon! Stay tuned for our fully comprehensive overview of the macroeconomics, presale, rental and resale market video report in the March edition of The Pulse.